Negotiations on health insurance are a weight around our neck at the bargaining table

Please support my work here by purchasing a subscription if you can afford to do so. If not please subscribe for free!

I don’t know what my fucking yearly deductible is right now. I have certainly known what it is at many other times in my life like literally a couple days ago when I got a fucked up bill I mentioned in here but at this current moment I am at a loss it’s like how you know what the capital of Chile is but depending on when someone asks you you might not be able to access that information in your muddy brain water. After thirty minutes of looking I can’t seem to find my deductible on the Harvard Pilgrim insurance website. I can’t find the deductible or anything about Chile whatsoever. Wait what is the difference between a deductible and a premium and out of pocket expenses again? Surely we all know but sometimes we forget.

I am reading the statement of benefits handbook but it’s eighty eight pages long and a schedule of benefits document which is a mere eleven pages long but nowhere do they straight up say “here’s your deductible bitch.” Ok wait it does say my yearly out of pocket max is $5,000 and our yearly family max is $10,000 and I guess compared to some people that’s not terrible (?) but it’s not hard to imagine a serious accident or illness that would dump all of that on us at once fucking us real good.

I think we can all agree it’s very good that you have to read almost one hundred pages to figure out whether or not getting sick is going to bankrupt you or merely cost your rent payment for the month.

We have pretty ok insurance I’m told. We get it free through Michelle’s work where she is a teacher and by get it free I mean we pay $500 a month for it. That’s what a premium is. Every year or whatever it is they go back and negotiate this shit as a union and the thing you sometimes hear from people with union jobs is that they worry about giving up the good insurance they fought for. Actually you hear that sort of thing more often from the likes of Joe Biden and Pete Buttigieg and other craven Democrat sellouts who use fear to convince people who have it pretty ok that they will have it terrible if everyone in the country gets to the baseline level of pretty ok that they are at. The thing is though if they didn’t have to spend time bargaining for health insurance unions like Michelle’s or whoever’s could spend more time bargaining for better wages and working conditions and other things without the prospect of diminishing health coverage looming over their heads like an executioner’s sword.

I was thinking about all this because of the story about the Culinary Union representing 60,000 casino and hospitality workers in Nevada and their leadership’s recent attack on Medicare for All which has been a whole fucking thing but probably isn’t worth getting into the weeds on here except to say as always the most craven operators in the Democratic party are lying to its rank and file that better things aren’t possible. Also it all somehow revolves around Bernie Sanders supporters being mean to Neera Tanden and her friends online which is the single more important issue of our times.

Read some more on whether or not the Nevada Culinary Union actually has “good insurance” or not here from the People’s Policy Project.

Journalists covering this story almost unanimously repeat the line that the union currently has incredibly good health insurance but then fail to provide any specific details about it. In reality, the union’s health plan, like most other health plans, is not that great.

Premiums

For starters, the Culinary Union likes to tell journalists that their health plan has no premiums. But this is not really true.

For workers to get the premium-free coverage (meaning the employer pays the full premium), they have to work at least 240 hours every two months (approximately 30 hours a week). Workers that put in fewer than 240 hours are required to self-pay $4.74 for every hour below 240. This means that when workers put in fewer shifts, they not only bring home less income, but also have to shell out potentially hundreds of extra dollars to stay insured.

Part-time workers, which are many in the hospitality industry, who cannot afford to pay their way into the union insurance find themselves in a particularly messed up position because their hourly wages are depressed by the employer insurance arrangement but they don’t actually receive the insurance that their foregone wages go towards.

Unsurprisingly this bought and sold fucking rat fuck Pete is lying to people about what Medicare for All would actually do and scaring them into thinking they somehow have to lose their insurance just because other people will be getting it.

The unspoken lie at the heart of Pete’s message is about the concept of “choice.” What we are choosing under his framing is not our own actual healthcare but which health insurance corporation profits off of us accessing that healthcare. We get to choose what middleman siphons off a significant portion of our spending.

“So many great choices!” one person replied to Mayoral Peter. “My choice is to pay $900 a month in premiums in order to get to pay a $6,000 family deductible. OR, I can pay $750 a month for a $12,000 deductible. What person who isn’t actively profiting from it would ever want to keep this system in place.”

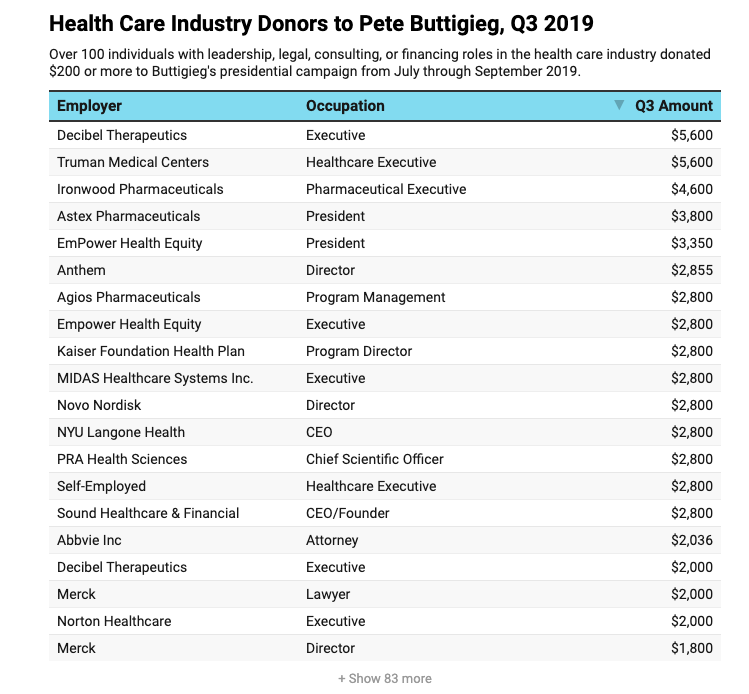

Buttigieg (and Biden!) you will not be surprised to hear are absolutely rolling in donations from the healthcare industry as Sludge has documented.

Side note but what is this “affordable” slipped in here by Liz by the way? That affordable is a load-bearing proviso opening an entire realm of shitty potentialities.

Back to Pete’s lie though.

Incidentally under Bernie’s plan for Medicare for All the invested labor into securing healthcare is reckoned with.

A fair transition to Medicare for All: Bernie will require that resulting healthcare savings from union-negotiated plans result in wage increases and additional benefits for workers during the transition to Medicare for All. When Medicare for All is signed into law, companies with union negotiated health care plans would be required to enter into new contract negotiations overseen by the National Labor Relations Board. Under this plan, all company savings that result from reduced health care contributions from Medicare for All will accrue equitably to workers in the form of increased wages or other benefits…

The replies to Pete’s posts are filthy with union workers telling him to go fuck himself (so rude right?) but I wanted to hear from a few more about how the healthcare they negotiated actually works for them and here are a few of their stories.

- I'm in a union and the private insurance option I chose lol (meaning I had to take because it was the only one of the three options I could afford) was a family plan with a $7,500 yearly deductible. That's the union member freedom to choose guarantee baby! Good news is though, once I simply had money taken out of my check every month and then paid $7,500 everything, was 100% covered! Until the following January, then it's time to find another $7,500 haha! Having medical insurance tied to employment is insane. Medicare for All now.

- I am union, but I don't understand any of the insurance. My cheap plan deductible is $6,000 per family, or $3,000 per person, and I pay $100 a month. Not great, but could be worse I suppose.

I’m a union negotiator and I recently bargained a contract where we stopped increases to employee healthcare contributions as best we could. In the previous one, which I didn’t negotiate, they went up by 7% in three years, and in this one they only go up by 2% in four years and not at all in the first year. But since premiums went up, which I have no control over, I had employees go absolutely ape shit and resign their union membership. It didn’t matter that I explained over and over how the union can’t negotiate premiums directly. Healthcare is an albatross around my neck.

I work in the public sector, so this may not be universal, but I know that my employers hate bargaining healthcare too. It’s a huge drag on them.

Medicare for All would 100% eliminate these headaches. My issue is that union members, understandably, don’t want to move from their Preferred Plus coverage to a high deductible plan, but the amount of bargaining power it takes to maintain these god-tier plans gets bigger and bigger every contract. And even when we can slow the increases as well as we can, it still isn’t enough. The problem is the system.

I would have so much more room to push for wage and retirement increases if I didn’t have to worry about treading water on healthcare, and I can’t ask someone to drop down to shitty coverage in good conscience. I have health issues myself. It’s one reason I quit teaching college to work for a union.

I’m glad the culinary folks have that good shit, but god damn I hate my “good union insurance.” I work for a union hospital in upstate New York and I have a $2,600 deductible. My employer pays the $700 a month premium, but we have to pay out of pocket for the dental and vision premiums if we want that coverage. That might sound decent, but most hourly employees who aren’t nurses make less than $30,000 a year. If you have a spouse and a kid the deductible goes up near $10,000 a year and you have to pay their premiums to get them family coverage. It is basically impossible to put your family on the plan and a good number of people have to apply for state subsidized insurance for their kids.

If my employer doesn’t have to pay $700 a month for me, our bargaining committee could get that money back in wages, and we would not have to spend tons of time arguing about insurance plan details while at the table. My coworkers with kids already use state insurance coverage for their little ones, but have to renew it every year with paperwork and income checks. I work for a damn hospital and people get punished for having kids.

Negotiations on insurance are a weight around our neck at the bargaining table.

- I was a Teamster until a few weeks ago due to a job change. It's the same shitty insurance options everyone else has. About six months ago my dentist told me I had a growth on my tongue that needed to be biopsied. I called the insurance for referrals, and there were only three I could get to. I called them all, and each said they'd stopped taking my insurance. Finally I went in to see my PCP, and he was like, “lol you just bit your tongue hard and it grew back weird.” It was funny in retrospect, but I didn't really appreciate having anxiety for two weeks. I mean, I understand humans don't like change in general, but I can't wrap my mind around thinking the current system is fine. The shit I've dealt with is mind numbing, and it's been for relatively minor issues. I can't imagine what it would be like for something serious.

I realize that in telling this story I should at least acknowledge first that from any outside perspective it would appear that my wife and I are lucky to have what is termed “good health insurance” through our respective jobs, but this is what good insurance gets you.

My wife had a baby at one of the better hospitals near us on December 31, 2018. Despite the fact that she was in serious labor from around 10 PM on December 30, the nurses held off on admitting her until midnight, as they said that would give her a little additional time in the hospital. She had the baby in the early morning on the 31.

Her health insurance was through the company she worked for. On January 1 2019, her company changed their health insurance provider from Company A (one of the “better” ones), to Company B. We knew this was happening ahead of time and asked the hospital finance department if this would be a problem and they said no, it would be treated as one stay.

The birth was totally normal, no c-section, healthy baby, and we checked out on January 2, typical 48 hour birth stay.

In February 2019 my wife got a bill for around $14,000 from the hospital. The hospital said that Company A declined to cover the charges on the grounds that the stay lasted until Jan 2, and Company B declined to cover the charges on the grounds that the stay started on Dec 31. All throughout 2019 my wife kept getting bills for random amounts from the hospital, sometimes $10,000 then $6,000 then $600 then $4,000. She fought with both insurance companies until the summer, when she got a health insurance advocate (a thing I never knew existed) who was supposed to resolve it.

It took until November 2019, eleven fucking months, for the bills to stop. She ended up having to pay $1,000 to each health insurance company because they both said she at least needed to pay their respective deductibles. Eleven months of stress, collection phone calls from the hospital finance department, repeated hours-long phone calls with two separate health insurance companies. It was insane, and we’re supposed to feel lucky that we can afford this insurance at all.

I used to be in the Army, which means I had Tricare for eight delightful years. Tricare is the best insurance you can get in America, precisely because it is socialized. All the young and fit soldiers are subsidizing all the old and sick ones, but the young fit ones benefit too because everyone is just....covered. Doesn’t matter if you’re injured, doesn’t matter if you’re sick. I was hospitalized a month out of Basic and was bewildered when I checked out that I didn’t even have to fill out paperwork. They just looked at my uniform and said “You’re all set.” I would happily give up any private health insurance, including ours, for M4A if it is like Tricare.

This person isn’t union but the same fear mongering about “losing your insurance you get through work” applies.

- I work at a restaurant. I’m not in a union but I have insurance through my company. We were bought out by a much larger company and they changed the weekly average minimum hours needed to qualify from twenty five to thirty five. The thing is that nobody works for or is even scheduled for thirty five hours, and in fact they have been aggressively cutting hours. All of a sudden I don’t have insurance after three years with this company. Now I basically have to look for a new job solely for insurance purposes. Meanwhile I’m happy where I am now and don’t want to leave. This affects like 90% of front of the house people where I work.

Ok so those are all kind of bad but here’s a real bad one.

About a decade ago I was given a job that put me into one of the major entertainment guilds. All anyone would say to me is how great the health insurance was! This is the sort of insurance that people would pick if they could pick their own insurance. As my wife and I were expecting our first child this was great news.

Over the last ten years, our health insurance has been... pretty good. I don't want to complain, given the situation that so many others are in with worse insurance or no insurance. But through the birth of two kids and standard family maintenance, we've run into various bureaucratic headaches and nonsense with our policy, all of which seems to be standard to the insurance experience, but nothing worth noting to a reporter or news outlet.

But a year ago I was diagnosed with cancer and now we get into the good stuff.

Since then my primary job has been to endure surgeries, chemotherapy, and the vagaries of cancer treatment, in addition to trying to work to help keep my great health insurance, as well as parenting our two kids.

My wife's job has been to help manage the emotional weight of that treatment, the incredible load of appointments, and all the insurance and billing. The last of which is its own job, along with her own full time job, on top of parenting our two children.

From the beginning we've been dealing with insurance rejections and claims for things that no one should have to deal with. While I was in the hospital being diagnosed, they sent a sample off for genetic testing. As my cancer wasn’t “age inappropriate,” there was reason to believe that I had a genetic mutation that was causing this cancer, and if that was the case, I may be eligible for a pill treatment that was in clinical trials.

The good news? Testing revealed that I did indeed have the genetic mutation that caused this, and I will qualify for this pill treatment. The bad news? Insurance rejected this genetic testing as it did not, “impact the outcome.” Leave it to the insurance industry to find the darkest joke in this whole disease.

That began our pile of unresolved or contested claims. After surgery, I was prescribed physical therapy within my hospital. Two months after PT ended, our insurance company wrote to say that they would cover $50 a session for session that cost $600.

As chemo began I was told that anytime my temperature got over 100.4, I had to go to the ER at the hospital. This past summer featured a run of four hospital visits for fevers, pain, and illness. The last two were rejected by health insurance. We were able to get them reversed, but is this how we want to spend our time when we could be working or being a family?

Two weeks ago I needed to get one of the eleven meds I'm currently taking refilled. I went to the CVS on the corner, and they told me that it was going to cost $140. Why's that?

“Eh, probably because it's the beginning of the year and deductibles are high.”

My wife didn't believe that answer, so she called insurance and her instincts were right! This was deemed a “maintenance medicine.” So, if I got it refilled for one month, it costs $140. If I'd gotten it refilled for 90 days, it would cost $25. We returned the initial refill, but to find a pharmacy that either 1) had enough pills for 90 days, and 2) was qualified for use as a “maintenance pharmacy,” took eighteen phone calls. Eighteen!!! It was an entire afternoon's work. And I still only have half the meds.

Our next impending nightmare? Because I have this genetic mutation, I may be able to take a pill to treat this. But the pill is only available through FDA trials, as it has not been approved for final use. So my oncologist is petitioning to get me to take this “off label.” Which is us trying to avoid having to pay $22,000 a month for the pill. We'll see how that all sorts out.

But keep in mind, every minute our doctor spends writing those letters, or dealing with our billing questions and complaints is a minute he isn't practicing on me or one of his other patients. Is this what we want doctors doing? It seems a terrible use of their time, on top of wasting mine and my wife's. This whole system seems feels set up for one group: insurance companies and their shareholders.

Again, I am one of the lucky ones. I have, ostensibly, good insurance, and I have an educated wife who can help with the burden of this, who speaks English as a first language, and who is a skilled organizer. But what if you don't have her? Or any of the myriad disadvantages that could pop up?

It's a lot, but at the same time, I've gotten more time with cancer than most do, and as frightening as it is, I'm better positioned to deal with it than many, many others. And that's what is most terrifying to me. I don't understand how anyone receives treatment at this point. I do understand every article about how most Americans are one bad diagnosis or billing cycle away from insolvency... That looks very believable from my vantage point.

The idea that this is all, somehow, worth fighting for is comedy of the highest order, and the only reason I can possibly see as to why you'd fight for it is that you are profiting off it (Pete/McKinsey/lobbyists). And the only reason I could see someone voting to keep it is fear of the unknown. Sure, switching to Medicare for All or single payer will be an overhaul and grind some gears for a few months. But nothing is more wasteful or less efficient than whatever this Frankenstein's monster we've created is.

Rage Against the Machine tickets went on sale yesterday and I guess you have to pay like $1,000 for them which is sort of funny. If you missed this old Hell World it’s about seeing them for the first time at my first ever real concert and about Vietnam and Amazon and some other things. It’s “one of the good ones.”

I was thinking about the photo of Quang Duc this morning because I just read a piece in the New York Times Magazine’s Letter of Recommendation column about the band Rage Against the Machine and I remembered I had printed out a photo of the cover of their first album which showed him burning to death and that just about blew my mind as a teenager. I thought it was the coolest thing I’d ever seen so I taped it up on my wall. Not cool but you know what I mean. The sincerity of it.

In the piece Jonah Weiner writes that he first learned about Quang Duc and a host of other protests and instances of government corruption from that album which is also true for me and then he wrote something that I think about sometimes about how we have to convince ourselves at some point as we get older that being pissed off about that sort of thing is somehow the realm of misguided youth like it’s immature to walk around fucking rip shit all the time about how people are being taken advantage of by the powerful and always will be.

Alcohol makes me mean and depressed and a fat fuck but on the other hand it also feels good for like thirty minutes tops one out of every five times so we have no choice but to stan. To be honest I don’t even really mind the depression and the nihilism it engenders in me my efforts to cut back lately are primarily about the getting fat part. In order to temper things I’ve become a Weed Guy recently and it’s fine and nice and everything but now I have the problem where I smoke and then eat an entire thing of these little bitches.

Just saw that Jacob Thiele the longtime synth player for The Faint died. A supremely underrated band. Someone said he had struggled with addiction issues but I don’t know if that’s true or not. It probably is.

Just went into a The Faint YouTube hole and it brought me to Does It Offend You, Yeah? another great 2000s synth-punk band.

I thought this was a pretty good piece on Slate about the difference in how the vile “Bernie or bust” people are treated compared to the benighted mythical swing voter.

There’s another consideration here too: Because folks at the center tend to be wooed by multiple candidates, they’re used to having options, and they’re used to the experience of their vote determining who ends up with the nomination. This means that they usually like the candidate they vote for, in the primary and in the general. Not so for leftists, who get to merely tolerate the candidates they end up having to vote for in order to mitigate the damage from a worse result. Now, with Sanders’ New Hampshire victory confirming that he’s the one with the best shot at winning this thing, the reverse might obtain. For the first time, it might be voters in the middle, not leftists, who have to hold their noses and vote for candidates they don’t like who barely acknowledge them.

…

Every threat these Sanders stans are explicitly making is one the venerated Centrist Swing Voter makes implicitly—and isn’t judged for. The centrist never even has to articulate his threat. The media narrates it for him. “What does the swing voter want?” is the kind of question that rescues this brand of voter from owning or even admitting any moral consequences at all. The question is framed as sensible, and so is its subject. The swing voter—which, let’s be clear, is diminishing in this political landscape—is typically treated as the antithesis of a Bernie stan: as a rational and passionless subject (as if contemplating just not voting in an election were a morally neutral choice). That the swing voter is arguably worse than the Bernie or Bust crew—in that in lieu of just staying home and not voting at all, he might actually vote for the other guy—doesn’t even register. That’s how accustomed we all are to being held hostage to the centrist concerns. As for leftists, who are undeniably real? Well, the Democratic machine has never wondered what they thought; it’s simply taken them for granted. After all, who else are they going to vote for?

Here’s me in the Guardian just now on the state of ethical reclining under capitalism. Read the whole thing here.

…In the face of such conditions, on top of all of the other nightmares of the flying experience – from authoritarian security theater at the gates, to the increase in cost, and the slow removal of courtesies that were once taken for granted, like meals and actually being able to bring luggage with you – it’s no wonder people are nipping at each other’s throats.

But this isn’t necessarily of flaw of capitalism, it’s the entire point. Rate of passenger irritation is merely a data point for airlines trying to determine where the line between customer hardship and maximum profit is. No doubt much expense has gone into drawing up actuarial tables pinpointing, down to the last millimeter, the difference, when it comes to our seats, between a tolerable experience and a torturous one.

Falling short of seizing and nationalizing the airlines, or dismantling capitalism as we know it, which are indeed worthy goals, it would behoove all of us, the straight-backed bathroom adjacent flier, and the luxuriating recliner, to keep in mind where the real ire belongs here.

Capitalism pits us against each other, convincing us that it is our comrades in coach that are responsible for our own misfortunes – when that is almost never the case. It’s the powerful who conspire, like parasites, to suck us dry. And as long as we’re scrabbling over scraps with one another, it keeps them off of our radar. If we ever figured out how to work together in solidarity, think about how high we could fly.

OK BYE